Personal vs Commercial Lines

I’m often asked if the Ignite Broker policy admin system “does” personal lines or commercial lines. Answer: it’s the wrong question. Let me break it down for you

P vs C: is there a difference?

Simply put – personal lines products are sold to individuals and commercial lines products to companies. To that extent they’re different. And commercial products are sometimes perceived as more ‘complex’ but is that true? In fact, to my mind, personal and commercial products are very similar, and there is a better question to ask when it comes to compartmentalising lines of insurance.

What are the key differences?

Commercial products tend to be more ‘complex’ in question set and placement because there is more variety to companies than there is to pets and their owners. Commercial products can also involve multiple insurers, payments direct to the insurer, and referrals. Personal lines products tend to be more price-sensitive and therefore have more point-of-quote enrichment, complex rating tables, and e-enablement.

Having said all that, there are also price-sensitive commercial products and complex personal products with bespoke underwriting.

Open market rates

There is one key area in which some systems can be said to be either commercial or personal lines-based. That is when it comes to Open Market Rates (OMR). A small number of large (and old/established delete as preferred) software houses have built up a large panel of OMR in their particular area of expertise (i.e. commercial or personal lines). For OMR commercial lines go to Acturis (https://www.acturis.com) and for OMR personal lines SSP (https://www.ssp-worldwide.com) or OpenGI (https://opengi.co.uk). These companies do this stuff well.

I am of the opinion that OMR are increasingly insignificant but that’s a blog for another day…

So is Ignite personal or commercial?

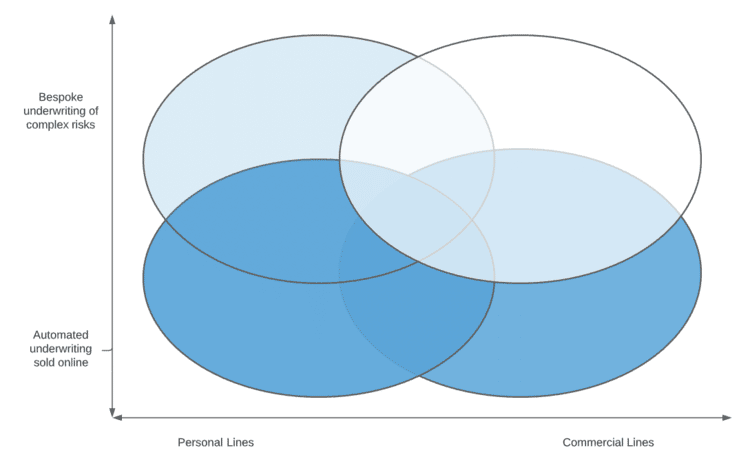

Coming back round to the question, Ignite does both personal and commercial lines, but only of certain types. Here is a sort of graph + Venn diagram to illustrate the point:

Ignite’s true sweet spot is in automated underwriting sold online (low on the y-axis). We predominantly do personal lines, because more of those products are e-enabled and traditionally fit a larger market. Having said that, Ignite is increasingly involved with SME, Cyber, and other less bespoke-underwritten commercial risks.

So can there be a cross over from personal lines into commercial lines? Absolutely! And there is great benefit to doing so: all of the learnings from complex online personal lines risks (e.g. streamlined customer journey, enrichment, automation, etc) apply to commercial too.

I suppose the conclusion is that, if you’re looking for a system for commercial products, see if you can’t find yourself a personal lines one!