The journey to Artificial Intelligence in Insurance

4 May 2021

There have been a bunch of crazy developments in the field of Artificial Intelligence (AI) in the past few years. Google’s AlphaZero beat the leading Go player in 2016 using techniques called Neural Networks and who knows what they’ve achieved in the 5 years since. If you’re interested they publish most of it here: https://deepmind.com/

This blog isn’t really about AI though, it’s about the journey that companies need to go on in order to achieve AI-readiness.

What is AI?

Artificial intelligence (AI) is intelligence demonstrated by computer programmes that mimics human-style intelligence such as learning and problem-solving, as opposed to more traditional ‘computer’ skills of calculation or processing.

Why is AI relevant for insurance brokers?

AI has wide relevance for almost all spheres of industry, but insurance particularly because of the vast amount of data and variables available to analyse. Healthcare has seen a huge surge in AI investment in recent years and it is inevitable that some of this will trickle down to insurance products, journeys and pricing too.

What are the stages to get there?

Most businesses are a long, long way off achieving AI. But there are steps along the journey that they can be making.

Data Access

AI feeds off data. Access to data is therefore mission critical the beginnings of any AI venture. Companies should ensure that their data is readily accessible, structured, and as full as possible to make the most of it, now or in future.

Data Analytics

Humans are good at problem-solving. Better than most machines. Once data has been assembled there are good tools (like PowerBI or QlickView) for visualising it. Businesses should layer such tools onto their data warehouses/lakes and make the effort to analyse the results of just looking at trends and correlations.

Machine Learning

Machine Learning (ML) is the step between looking at an Excel spreadsheet and AI. ML is not ‘intelligent’ in that it needs to be told ‘what’ to do, but it can do what it is told to do better than a human can. ML, properly trained, will notice correlations within data that the human eye cannot spot: it will see multi-factor or multi-dimensional correlations for which there are no easy visualisation tools. Microsoft Machine Learning provides an excellent toolkit for such projects. Building supervised learning algorithms will likely require an experienced or trained data analyst or programmer.

Artificial Intelligence

Once these initial steps have been taken, the door to real AI is open.

Very few insurance companies truly stand at this hallowed portal as yet, but for those that aspire to do so, the previous steps must all be taken. And there is great benefit to be had for the business and its’ customers in doing so.

Benefits of losing your legacy system

14 April 2021

What are legacy systems & why are they bad?

The term legacy system gets bandied about a lot. Exciting new insurtechs view any technology not created in the lasts 5 minutes as legacy. But that’s not the whole truth of it. A legacy system should describe any technology that consumes lots of time in processing workflows or general administration and is difficult to update. In the language of insurance, a legacy system is one that holds a broker back from finessing their existing products or launching new ones.

There’s actually some older tech out there that works very well and doesn’t really need to be updated. Legacy tech just describes systems that don’t work well, not systems that are old.

It should be easy enough to see why legacy systems are bad.

So why not change them?

Changing systems is perceived to be a major headache and business risk. This in itself is quite a dated view. Not only has technology improved in the last 10 years but so has project management and migration. The process of change is much easier than it is often thought to be.

Legacy systems, by their very definition, are holding businesses back. So changing them, and finding the bandwidth to change them, is critical. There are two key elements to consider:

- What do you want from your new system?Answer this by considering where you’re held back at the moment, but also looking to see what is out there. Try to be led as much by what new systems are designed to do (and find one that fits your business) than moulding the system around what you want to achieve.

- Data migrationData transfer is only as difficult as access to existing data makes it. The chief problem with data is not getting it into a new system, but getting it out of your old one. Even before you consider your new system, ensure you have good access to your existing data and do a data cleanse exercise to make sure you have key information such as email addresses for every record. Make this part of your client interaction scripts for a year beforehand to ensure you’re as ready as you can be.

Moving systems also doesn’t have to be a big bang approach. Pick a product or area that you want to change and do it gradually if that makes more sense.

What are the benefits of changing?

When you’ve implemented a new system to replace your legacy system you’ll have new challenges to focus on.

Your processes will be much more efficient and automated so staff that were engaged in admin will need to be repurposed and sometimes retrained. This can bring a renewed focus on quote-to-policy conversion to maximise marketing budget, or improved customer service. The end result will be better renewal retention and brand perception.

Your business development resource will also be freed up from BAU firefighting and can begin to look at new product lines and business expansion. Plan for this as part of your longer terms software strategy.

Replacing a legacy system is a daunting process but often easier than it first appears. If you’re being held back by tech then take advice from systems providers and start the transformation process.

2020 R&D Case Study

9 April 2021

What is R&D?

Research & Development is the time and effort we put in to bettering our product, future-proofing and securing it, and responding to the needs of our present and future customers.

Why do we do R&D?

We do R&D continuously because the market never stays still, and no software is ever complete.

New technologies (everything from file formats to security protocols) and regulations (from GDPR to the CMA) and ideas (brokers are an innovative lot) demand that our systems are adaptable and future-proof.

An R&D project from 2020 – New Rating Engine

Every year we review and update our product roadmap which includes a significant investment of time and resource into developing products and features that will benefit our client base. In 2020, one of those major projects was to re-write our existing rating engine.

Problem we’re solving

Historically, we would use developers to translate an insurer’s rating algorithm into code, but this was time-consuming and therefore costly.

Instead we wanted something that would remove the need for developers in this process, in order to reduce the time and cost of rate builds and updates.

How we did it

Our clients (insurers and brokers and MGAs) tend to deliver rating guides to us in Excel. So we thought – let’s use Excel. Sadly Excel alone isn’t powerful enough to compute the 100,000s of quotes we have to process every day so we researched and developed a tool that would convert an Excel spreadsheet into code.

Using Open XML we now have the best of both worlds: our clients can make rate updates in Excel without needing to learn new configuration tools, and at Ignite, we don’t need any developer intervention to upload them to the system.

Our CTO worked closely on this project with other developers in both our Manchester and Mysore offices and with our BAs and Testers over a period of a few months.

Result – metrics/screenshot

The results of this project have been excellent. Our build time for new schemes has been reduced by over 50%.

Rate updates now take place without a code deployment and can be done in minutes.

For our clients, this means their rate updates are done at zero cost and within minutes.

R&D plans for 2021

- MI App

- OCR

- Next-best-step

Digital Readiness

6 April 2021

What does it mean to ‘go digital’?

Going digital means giving your customers, staff, and management the widest possible array of online and data-enriched tools so they can achieve their aims in whatever suits them best.

How easy is it to achieve?

It’s not always easy. There are three major hurdles to clear:

- Your own mindset – prioritise digital transformation above all other concerns. Growth, client retention, and staff satisfaction will all stem from this.

- Your staff’s mindset – people are often resistant to change. Encouraging your staff to contribute and embrace change is a challenge in itself.

- Your technology – investing in systems that enable digital transformation is often expensive and a journey into the unknown.

What’s the end goal?

The end goal is that your customers can interact with the product and business in the way that they want; that your staff enjoy the benefits of automation of repetitive tasks and seeing their own feedback implemented; that your company is able to make better, more informed decisions and quickly adopt new strategies, technologies, and products as they emerge.

Stages on the journey

- Take a good look at your business, staff, processes, and clients. Be honest about what could be improved, where human intervention is necessary and where it’s not.

- Prioritise the results of your review.

- Assess the barriers to achieving each of the identified areas of improvement.

- Create a strategy/roadmap for increasing your digital readiness.

- Communicate this strategy to your staff and seek their feedback/input.

- Be bold and implement the changes, no matter how seismic or costly in the short term!

How to get started

Every great journey begins with a first step.

Get your key staff and stakeholders together, and begin the process. Allocate time and regular feedback sessions.

If you’re not sure where to start or would like support in starting your digital journey, just get in touch, or you might like to take our digital readiness quiz to find out whether you’re ready to meet the digital demands of 2021 and beyond!

No-code – speed & simplicity

15 March 2021

It is a common misconception that software developers dream in code.

Despite having more than a million lines of code in our platform, we actually dream of no-code.

What is no-code?

No-code is the term for a platform that allows non-technical system users the ability to setup and configure their system using codeless graphical interfaces. For an insurance platform this means that our clients can customise their own systems, rather than having to try to describe what they want and have it built by a bunch of guys in Star Wars hoodies. No-code implementations for our specialist brokers is a key milestone on Ignite’s product roadmap.

What are the advantages of no-code?

In short: speed, reduced cost, and simplicity. Systems can be set up by our BA team on the day of delivery. The setup cost is greatly reduced by removing expensive coding resources. And finally the simplicity of implementation negates the misunderstandings and complexities of scoping and translating requirements. No-code means that our clients get the entirety of Ignite’s large and sophisticated broker system implemented to their bespoke requirements in a matter of weeks not months or years.

Will our clients need to learn no-code?

No! It’s our belief that low-code or no-code should be part of Ignite’s arsenal, not a client’s. At present Ignite Broker clients can amend their question sets, pricing, documents, workflows, users, accounting rules, add-on products, etc… but in reality our expert team of BAs manage that for them. The result of no-code is that our brokers can focus on winning business, client relationships and profitability. System updates happen seamlessly in the background: quickly and low cost. Nice.

Low-code vs no-code?

There’s basically no difference. If you had to pinpoint one, it’d be that low-code admits it can’t do everything, whereas no-code pretends it can.

What is *real* self-service in insurance?

3 March 2021

If you dabble in the world of insurance software (and who doesn’t) then you’ll have come across the concept – and the promise – of “self-service.”

Self-service means that customers can do things for themselves online rather than calling a call centre. This is useful for everyone: customers don’t like talking to people (who does?) and they can manage their policy out of office hours; brokers don’t want to spend money needlessly on manning a call centre (at an approximate cost of £25-£30/call).

A few of Ignite’s competitors claim to offer ‘self-service’ portals, but in reality, few actually do. If they did, why wouldn’t everyone be using them?

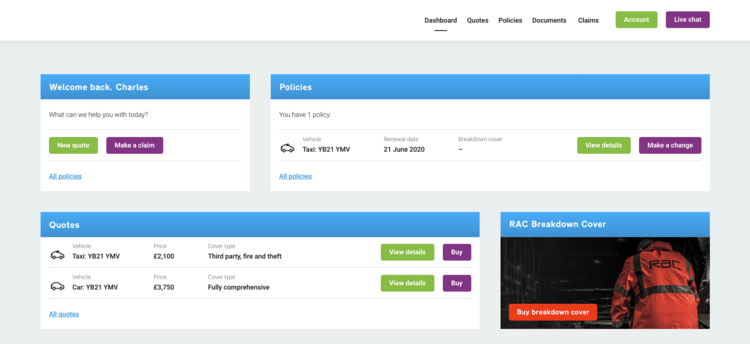

Here are a few features of the Ignite self-service portal. The ability to:

- Make changes (i.e. MTAs) of any sort

- Cancel a policy

- Renew a policy or manage the renewal by adding other details

- Purchase additional add-on products

- See claims

- View & download documents

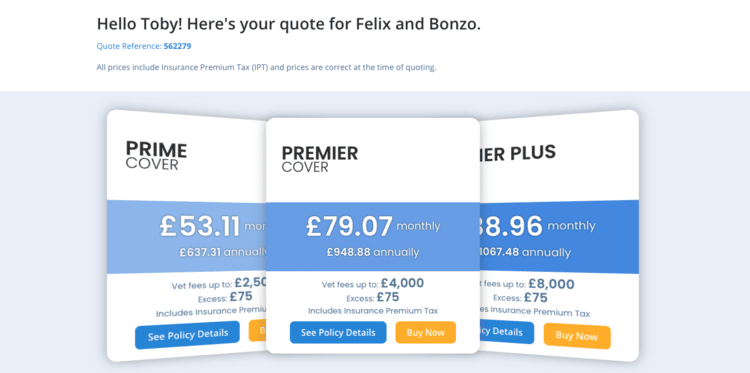

This is an example of what it looks like:

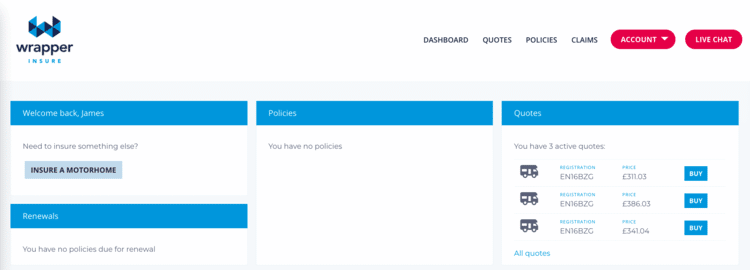

Customers who don’t have a policy can go there to retrieve a quote (this example from the recently launched wrapperinsure.co.uk)

It is important with self-service that it is both easy to use and offers a full range of functionality.

For example, my personal home insurance with Home Protect has a portal, but it is not pretty (see screenshot below), misleading (my policy looks as though it has been renewed twice) and only allows me to download my documents. This puts me off both the brand and the product.

A good self-service portal dramatically increases the number of clients a single broker operative can administer: from ~1,000 to over 10,000.

Customers expect self-service these days, so it’s now standard across all Ignite implementations.

Personalising the Customer Experience

24 February 2021

Getting customers to come to your website is one battle, but the war is only won once they’ve bought a policy!

A personalised, considered online customer experience is critical to improving quote-to-policy conversion.

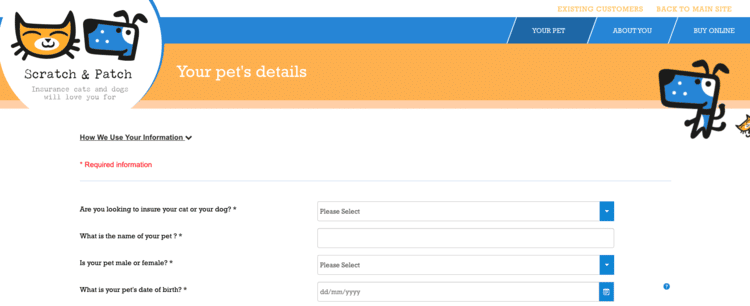

In late 2020 the Ignite team worked hand-in-hand with our long-term client, Scratch & Patch, to re-design and build a new client experience.

Since launching in 2015, Scratch & Patch had had a retro feel with this Rockwell font and blocky look:

While the quote-to-policy conversion rate was ok, it wasn’t spectacular. We knew it could be much improved. With this in mind, we worked together to create a new experience that puts the customer first.

The revamped site is slicker and smarter, drawing the eye to the required fields, and less dominant in the colour palette.

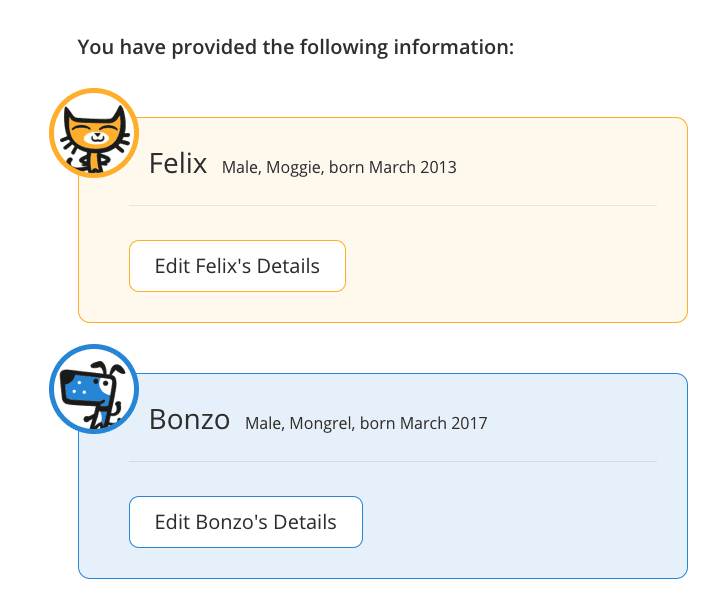

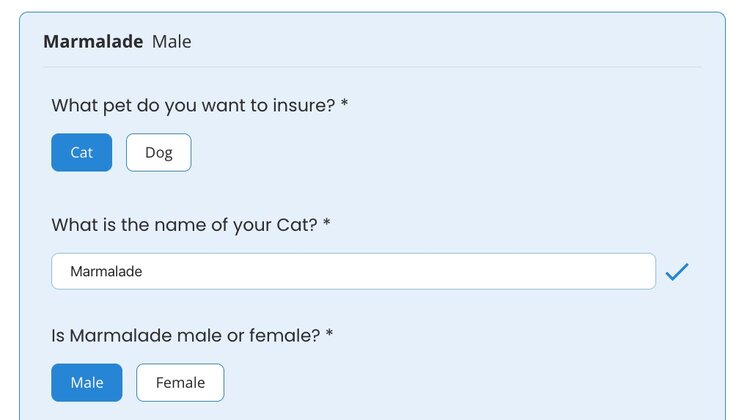

Most importantly, the entire customer journey is personalised throughout. Gone are the super-impersonal questions that refer to your furry friend as ‘Pet 1’ – now, as soon as your pet’s name is entered, we refer to them by their name from there on.

What loving cat mom (or dad) wouldn’t want to get Marmalade a policy that’s been made especially for him?

We achieved this using technology called vue.js which is now used across all Ignite’s brokers’ customer sites. Other examples are zoomcover.com and yoga-insure.co.uk

One of the beauties of vue.js is that it looks great on mobile, and also translates itself seamlessly into a smartphone app. All of which is great for Scratch & Patch’s customers who can now enjoy immediate access to their policies, documents, renewals, and claims in their personalised customer portals.

The build took around 6-8 weeks and we’re delighted with the results. The quote-to-policy conversion rate is substantially increased, and the customer reviews are excellent.

Have a go at getting a quote with Scratch & Patch here: https://community.scratchandpatch.co.uk/

If you’d like to see how we can apply these design principles to your brokerage then do get in touch.

Why brokers need to ‘bee’ more

8 February 2021

Here are a few business analogies drawn from the natural world: “busy as a beaver”, “fat cat”, and the business “unicorn”. I’d like to propose another animal-themed business idiom: “build like a bee”.

Follow me on this one. The humble bee makes its home lightweight, a flexible yet strong structure, versatile enough to grow quickly, changing shape and size depending on requirement. If a particular cell in a honeycomb isn’t working, a bee can quickly dismantle and put together a new, stronger structure.

The same should be true of business infrastructure

Many businesses are still inextricably tangled in complicated legacy systems. If one part of the system is no longer relevant or functional, or the business wants to change direction or integrate new, digital processes, it can be incredibly costly and time-consuming; with a high risk of downtime or business interruption, to break down and rebuild the system the way the business wants it.

There are many off-the-shelf products out there, and though it may appear quicker and cheaper to buy the full package and get started, buyers often end up with elements of a system they do not need or want and very little flexibility to do anything about it. Not very cost-effective.

This is the way it has “always been done” (our industry slogan?) and many companies are cautious about doing things differently. We work with a number of clients who prefer to stick with their legacy systems, we get it, and we have worked hard to ensure that we can integrate these systems with minimum disruption, but there is a better, more efficient way. A way that not only sets the business up for now but makes it future-proof with the ability to quickly respond to changes in the insurance-buying and consumption process.

Back to the bee

At Ignite we are seeing an increased adoption of a type of infrastructure that mimics a beehive; a total structure composed entirely of smaller modular elements, coming together to deliver a robust, resilient but most of all, agile result.

This microservice approach allows brokers to pick the specific elements of the system they need, combining best-of-breed modules to build a full front- and back-office, claims, and policy management system. In this way, modules can easily be taken out or added as needed giving the business the agility needed to quickly grow and respond to changes in the industry.

We have long been champions of this honeycomb approach, our Ignite Broker system is built in modular fashion meaning that our clients can choose all or some of the modules they need to build their perfect system; rating engine, customer portal, commissions, complaints, chatbot services – all discrete elements of our system that our clients can choose.

Benefits for the broking bee

This all might sound complicated, and dare I say it expensive, and that may be somewhat true. But in terms of long-term business growth, future-proofing and efficiency, it is the best approach for a growing business, and it isn’t as complicated as it sounds. Depending on your provider, modules can be easily slotted together and integrated with existing systems with little or no system downtime – all you need to do is work with your provider to carefully scope out the areas you need support, and they will tell you the best solution. Not just the off-the-shelf in-house solution, but an array of possible solutions to fit your business.

In a fast-paced, constantly evolving digital environment, most, if not all brokers could benefit from following the lead of the bee and adopting a modular approach to building their business, these are just some of the benefits:

· Pay only for the features you need rather than wasting money on system functions you may never use

· Quickly adapt and build on the system as the business grows and requirements change

· Minimal (or no) business interruption when different parts of the system need adapting

· Best of breed approach allows you to pick and choose the best modules from different providers

If you want to get building like a bee, we can help: Ignite Broker is a modular system that provides all the functionality you need in discrete cells that you can select based on your business need.

Get in touch with us today to arrange a free demo or have a chat about how we can help you.

FCA’s ‘price walking’ regulation and the law of unintended consequences

7 December 2020

In the 1970’s, US states began to require car passengers to wear seatbelts. Sounds sensible right? Unfortunately, immediately following this law there were more accidents, and though people were less likely to be fatally injured in an incident, the new safety mechanism of a belt led to more people adopting risky driving behaviours. Great (and vital) legislation, but who could have foreseen that particular consequence?

In September, the Financial Conduct Authority outlined its proposal to tackle concerns about dual-pricing in the home and motor insurance market. Following a lengthy market study, it found that customers were not benefiting from fair pricing practices, with renewing customers often offered much higher premiums than brand new customers on a like for like quote.

As part of its proposal, the FCA demanded that brokers offer the same price to both new and renewing customers, which on paper sounds sensible and most importantly, fair.

The premise is that those customers who don’t tend to regularly shop round for the best possible insurance quote are not discriminated against or penalised for their loyalty. If all goes well, this should mean that insurance customers won’t need to hunt around for the fairest price, brokers won’t frantically undercut each other to get new business and price comparison websites will have a greater focus on quality of product rather than price.

That might happen. But as with the US seatbelt legislation in the 70’s there may well be some unintended consequences. Let’s consider five possible scenarios arising from banning the seemingly destructive practice of price-walking.

A vicious cycle?

Competition in any market is essentially good for customers as it drives prices down and forces providers to innovate to make sure their offerings stand out to potential customers. Once the FCA bans price-walking, in theory all customers will receive the best possible price meaning they will be even less likely to shop around. Could this lead to innovation in the industry being stymied as providers rely on price-alone to attract and keep customers?

(Don’t) Go Compare

If customers know that they’re getting the best price both first time and at renewal, we are likely to see fewer customers visiting price comparison websites to hunt for the best prices on their premiums. The only problem with this is that price comparison sites need a good volume of traffic to make money to support their marketing budgets, and without it we could see them increasing their prices, a cost ultimately passed on to the consumer.

Fit for purpose?

If brokers are less able to win new business, some less professional ones may seek to regain their financial advantage by offering new ultra-stripped down, ultra-cheap policies that look good to the customer on paper, and in their monthly or annual statement, but on closer inspection may not give an adequate level of cover, leaving them exposed. In this scenario the customer will need to be ever more vigilant about checking their policy summaries and exclusions to ensure that in the event of a claim they aren’t left vulnerable.

Price-walking through a loophole

Brokers with profitable back-books will understandably want to keep their historically profitable customers. To do this we may see them making older products unavailable or difficult to find for new customers. This would then enable them to continue to offer a high price at renewal to existing customers whilst simultaneously launching insubstantially different policies for new business, technically price-walking as they could offer a near like for like product, but at different pricing levels.

Stalemate

Ultimately the market will see less churn, and I believe, less incentive for companies to provide excellent customer service to retain the business of their loyal customers. This could lead to less innovation to drive the industry forward in its quest to meet and exceed customer expectations, which given how far technology and our ability to provide exciting new digital solutions to customers, would be a great shame.

These scenarios could play out in front of us, or they might not, but one thing is certain, major regulatory change always has some unintended consequences.

What chatbots struggle with

13 March 2020

Ignite launched a chatbot facility early this year for our brokers. It’s been an eye-opener. People have come at poor old Iggy (the Ignite chatbot) with all sorts of puzzlers. Top entries include: “does it have like claims on it?”, “Am I going to France?” and “I didn’t receive the discount mentioned by Amber”. Amber doesn’t work for the broker. No one knows who Amber is. Let alone chip-for-a-brain Iggy.

Why do a chatbot?

Our clients – brokers – field lots of calls and live chat requests. Answering these queries definitely costs money, and only sometimes makes money. They’re also only available during office hours. So, to save the broker money and offer a 24/7 service we decided to set up a chatbot.

How do you decide what a chatbot should do?

To make the chatbot relevant to the broker we have them jot down the subject of their calls and live chats for a month, then categorise them by type of query. Those that can be automated (e.g. what is the cancelation fee?) are taught to the chatbot, and those that can’t we push through to the call centre.

How does the chatbot work?

Iggy is a natural language AI learning chatbot – if he doesn’t understand things we teach him how to respond until he can work it out for himself. The more we teach him the better he gets.

What functions does the chatbot do?

The chatbot’s primary function is to answer frequently asked questions. It can also interact with the customer’s data (if they’re logged in) to tell them details about their policy. It can direct the customer to the dashboard where they can amend, cancel and renew.

How good is it?

Iggy answers about 50% of all questions before they reach live chat or the call centre. Imagine that…a little helper that fields over 50% of all your calls. Could be handy that.

What does the chatbot struggle with?

Iggy is very good at noticing spelling mistakes, catching keywords and admitting when he hasn’t got the foggiest. He struggles with questions like these:

- “I’m not sure how much a quote is”

- “If my wife is pregnant can she drive”

- “Are you related to Yogi bear?”

You can only teach a machine so much…